Landlord life is one step closer

This train’s slow, but it’s not stopping.

It’s been one year since I started the process of becoming a landlord.

I’m not proud of the timeline. It’s taken me too long to cross the finish line.

I should’ve secured us a home by now. It should be cash-flowing, and it should easily rank as the best investment in my portfolio.

But I procrastinated on completing my biggest goal of 2024. Life played a part in delaying my progress. But my procrastination was largely due to my uncertainty. I wasn’t familiar or comfortable with the daunting steps required to initiate our home purchase. So I hesitated unnecessarily. Before I knew it, a full year passed.

I learned last week, however, that I had nothing to fear.

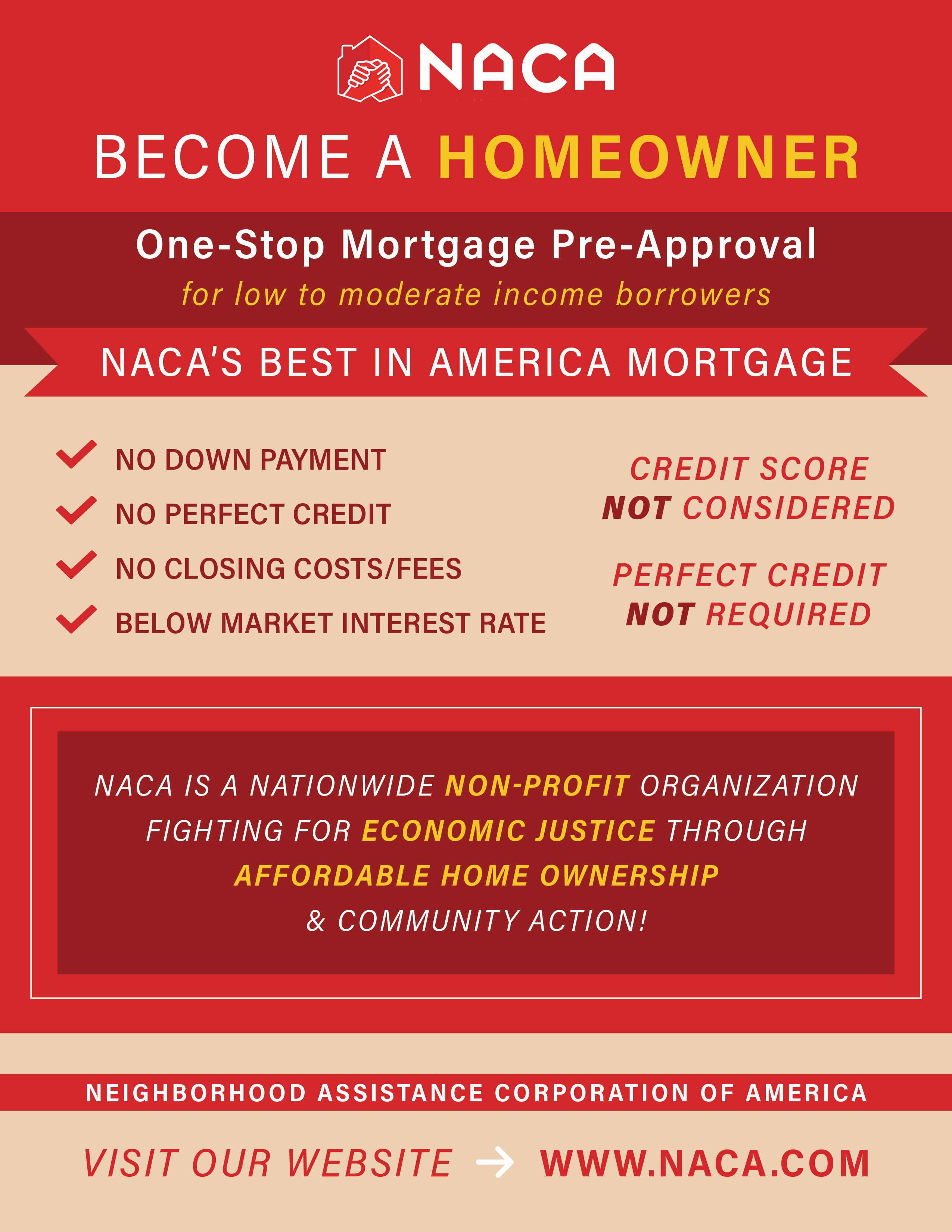

Last Wednesday morning, I had my long-awaited intake session with the Neighborhood Assistance Corporation of America (NACA).

My counselor, Marcela, conducted our meeting via Zoom. It lasted a little more than one hour. It was the next step necessary to get qualified to buy a home through this highly attractive non-profit organization, which provides below-market mortgage rates without requiring a down payment, closing costs or private mortgage insurance, all without factoring in your credit score.

It still sounds too good to be true. But it’s legit. The process, though, is as tedious as advertised.

Before I could book a pre-counseling appointment, NACA required me to complete more than a dozen tasks in its excruciatingly thorough portal. Because the organization offers such a sweetheart mortgage, it basically demands your life story. In no way is this a traditional home-buying experience.

I had to link all of my financial accounts and categorize every single transaction for each account. It’s by far the most demanding step, not because of its difficulty but rather the monotony and sheer time commitment. For example, that cloud storage that Apple charges you $2.99 for each month? That and other tiny expenses must be categorized each time they appear on your statement.

Not only that, but NACA requires tax statements and tax transcripts for the past two years, along with current W2 statements, proof of self employment, rental history and all debts.

Marcela, my counselor, went over everything in my file last week. Basically, her job was to verify all of my submissions and to ensure we were on the right track. Marcela was surprised that I had completed all that was required. She also marveled at how low my debt was and told me that the two of us will make a good team.

In the last half of our call, Marcela walked me through math using NACA’s trusted computations.

I was advised to think in the upper $400,000 range for a four-unit, multi-family home. NACA offers lower interest rates for lower income applicants who are deemed priority members. I earn too much to qualify for the lower 5% rate. We’ll likely be in the 6% range, Marcela said.

But I’m not swayed by interest rates, and I have a good reason to not be.

The national average for rent for a two bedroom apartment, Marcela said, is $1,650. That would equate to $4,950 a month in rent that we would collect. Yet I was told that my share of the mortgage would be $635. I’m still processing her information.

But if we’re collecting almost $5,000 in rent, we shouldn’t have to pay anything toward the mortgage. The vision then will start crystallizing as planned. Our tenants will be paying for our home. Money that no longer must go to rent or, soon, a mortgage, can be funneled to investments. The compound effect will get supercharged.

At the conclusion of our session, Marcela added nine more action steps that required my attention. They ranged from tasks such as providing proof of my child support obligation to explaning residential addresses that appear on my credit report.

One additional action step that Marcela didn’t mention during our session was the required multi-unit certificate requirement. Fortunately, I already knocked out that step in March. I’m ahead of the game in at least one regard.

I’ve already completed five of the additional action steps. The final four are at the top of my to-do list. And they aren’t a problem.

I’m no longer procrastinating.

Soon, it’ll be time to search for our new home.

Wow Darnell that’s awesome man, this sounds like the deal of the century!

Do you think you could speak more about the actual financials of the deal? How is that you’d pay $635 if you collect $4950 in rent but you’d pay $0 if you collect $50 more ($5000 in rent).

Happy House Hunting!!!